Our largest expenses are housing, food, and transportation. These things can be optimized and we will take a look at some options that may work for you. Then there’s the really easy ways to save- fixing those ongoing costs that you are paying too much for– like your cell phone plan, your cable, and your insurance. These are tips that will apply to most people but personal finance is a very personal thing. The things that my family have done to lower our expenses and save at least 50% of our income might not work for you. The best way to know where you can cut back is to take a look at your spending- maybe just start with the last 30-90 days and figure out where you could cut back.

Easy and Ongoing Expenses

These are really easy ways to save and will lower your expenses without affecting your lifestyle. Just set these things up right and start saving hundreds of dollars more every month going forward.

Phone

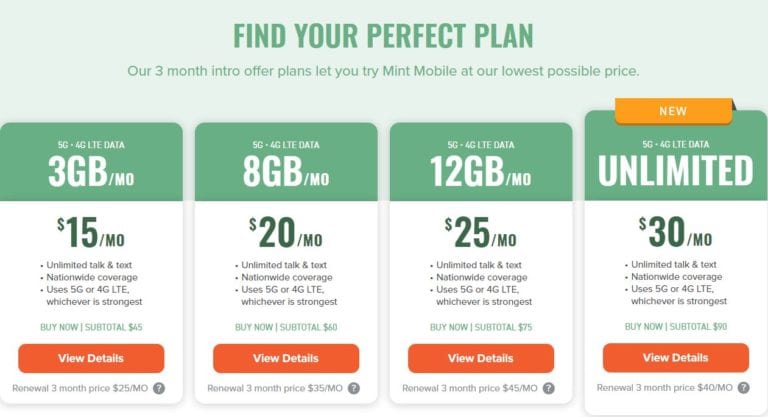

The average Verizon cell phone line costs $80 per month. We were Verizon customers since 2008 and when we finally switched plans last Fall, they tried to bully us into staying with them. It was completely absurd. I LOVE that we don’t have to deal with their sleazy customer service reps anymore. We kept our phones and just switched out the sim cards with the new company. Now instead of paying $170/ per month with sleazy Verizon we pay $50 per month for an unlimited plan. Honestly it’s more than we need and I’m planning to downgrade our plan again. With Mint Mobile you can get 3GB of data for $15 per month. Keep your current phone and your phone number and they don’t even charge for the new SIM card.

Insurance

If you haven’t shopped around for car insurance lately, you could be passing up hundreds of dollars per year in savings. Nerdwallet compares average costs of the largest insurers here.

There are many insurance options out there that are a total racket so it’s worth taking a look at what you have “covered”. We have lost a lot of money on insurance products that we don’t need and aren’t right for us- like whole life insurance. Products like whole life insurance are intentionally confusing in order to hide fees from the customer. You probably only need life insurance if there’s someone that’s counting on your income- a spouse or a dependent. The goal of life insurance is not to make someone rich if you die, it’s to help relieve some of the financial burden of your loss. Once you are FI, you don’t need to pay for this anymore. It’s a good idea to have health insurance but it might be worth comparing how much you’ve been using it to see if you could get the high deductible plan and stop paying so much every month. Healthcare.gov has a nice tool which will help you see whether your prescriptions are covered by each plan and helps you determine your costs out of pocket.

Entertainment

I keep getting these promotional ads offering basic cable for $59 per month. I guess that’s a discounted rate? First of all, this is a completely unnecessary expense category, there are tons of free options that will add to your happiness and enjoyment of life as well as your self development. Get a library card and download free digital and audiobooks straight to your phone or check out an actual book. Or you could get off your ass and do something actually fun like go biking or hiking or swimming. It’s good for you. If you also want to watch tv and films, you could spend way less than $59 per month and get it through Netflix or if you already have an Amazon Prime subscription, the Prime Video service is free and has more than enough quality programming.

I hadn’t realized this until recently but people pay $70-100 per month on games and gear. Admittedly, I am quite unaware of the gaming culture- despite my otherwise level 20 nerd status. I do know that you can completely cut this cost out by just playing free games- the quality can be pretty great. Mr. Nerd recommends this one.

Bank Fees

We don’t pay anyone anything to manage our money. Learning to manage your own money could save you millions of dollars over the course of your lifetime. Most financial advisors are commission based and they make more money on selling you on products you probably don’t want- but are too confused to realize it. And if you’re doing it right, it is stupid simple and won’t take long to learn. Here’s a short article laying it out.

We don’t ever pay late fees or ATM fees or anything like that. Fuck that. Find a bank that works for you– they are already making money off holding your money in your account- you don’t need to pay them fees on top of that. Our retirement accounts are all with Fidelity so that we can buy their zero fee total market Index funds FZROX. We really like Chase for it’s credit cards– but unfortunately they don’t service Hawaii residents for checking accounts. We have had good experiences with USAA and Wellsfargo as well.

The Big Three

Housing

In Hawaii it’s common for households to pay about 50% of their income on housing. This is significantly higher than the mainland where traditional financial advice suggests paying about 30% of income on housing. Either way, you’re probably not going to reach a savings rate of 50% or more if you are paying 30-50% of your income on a place to sleep. Instead I just try to get all my expenses as close to zero as possible- our mortgage is $1500 per month so… there’s room to improve. The problem with budgeting expenses by assigning arbitrary percentages of your income is that it encourages lifestyle inflation. The logic is as follows, “If you make $3000/ month then you should get a $1000/ month mortgage or rental. On the other hand if you make $9000/ month you should get a $3000/month house.” This is nonsensical. If you can live a good life on $2000/ month you should do that and save the extra for your future.

Househack

Househacking at a basic level is finding ways to cut the cost of your housing. This is really about turning a cost into an asset or at least minimizing the cost. This can mean renting or using airbnb to rent out any spare bedrooms. This can even be moving to a less expensive city and using geographic arbitrage to lower your housing cost. This can also mean buying a multi-unit home like a duplex and letting the rent pay for some of the mortgage (apparently there are rental market’s where the rental income would cover the whole mortgage). It’s pretty common in Hawaii to convert a carport into a rental. This may be a good option if you are handy and can do most of the work on your own. Be sure to get it approved by the local planning department before you begin construction or you may have trouble recouping the improvements when you go to sell your home in the future.

My favorite house-hack is the slow flip- wherein you buy a house with the intention of living in it while fixing it up to sell for a profit after 2 years. This takes advantage of the tax rule that allows all profits from the sale of a primary home that you have lived in for at least 2 years are taxed at 0% tax rate. There is a three-fold benefit to this, your mortgage payments are a long-term capital gains investment rather than a cost like paying for rent, any work you put into the house will help to increase the value of the home, and as you own the home, the value of property is also likely increasing.

Real estate appreciation rates are extremely variable and can be in the negative when accounting for the inflation rate. If you are thinking of getting into real estate, there are a lot of factors to consider to make sure you end up ahead. Here’s a good article from Millenial Money that will help you determine if this is right for you.

Food

Cook for Yourself

Learning to in-source your food preparation is probably one of the most valuable skills you will ever learn. Americans spend more on eating out than on groceries. The restaurant food markup is on average 300% (ranging from 155%- 636%) so for every meal you prepare for yourself at home you are paying about ⅓ of the price you’d pay at a restaurant. Homemade food is usually healthier and you can control the portion size which can benefit your waistline and your health.

If you need motivation to figure out how to cook at home- just take a look at what you’ve been spending on restaurants. In one month last year we spent more than $700 on restaurants- for two people. We’ve paid less than that for rent. Meanwhile we didn’t have enough cash to contribute to our IRA’s in 2018. Since getting our priorities in order, it only took us 4 months to max out our IRA’s for 2019 and 2020. Now we are working on and HSA and a 401k.

At first we starting just cutting our restaurant spending to $50 per month. That was really hard for us- which seems silly now because we hardly think about eating out any more. Here’s a great site for simple, fast, and low cost recipes.

Food Waste Sucks

We also had an issue with our grocery spending. I would buy way more than we needed and our pantry was way over stocked. Inevitably we would end up wasting food. Food waste sucks. It’s bad for your budget and it’s bad for the environment. I’m pretty sure it doesn’t directly affect starving children in Africa though. If food waste was a country, it would be the third largest greenhouse gas emitting country, behind China and the US. Wasting food is bad. So let’s just not do it. To avoid wasting food, I keep a close eye on the perishables and I plan what to cook based on what we need to use first. If I made more of something that we want to eat in a few days, I put the extra in the freezer. Then a couple weeks before I make a trip to costco I inventory the freezer and see what we can use up to make space and find some tasty way to use it.

The more time you spend cooking at home, the better you’ll get at it. The more recipes you get under your belt, the more comfortable you’ll get with finding creative and tasty ways to use ingredients. Home cooking becomes a money-saving super power especially when you call on help from Super-fabs!

Transportation

Getting from place to place doesn’t have to cost anything, yet this is often people’s second or third largest expense. So there’s a lot of flexibility in this line item. Some options include:

- Moving to a place that is within walking or biking distance to your work and a grocery store.

- Finding a way to work from home- full time or part time.

- Switching your fancy gas guzzler for a fuel-efficient used vehicle. Don’t buy new. Let someone else pay for the first 20,000+ miles of depreciation.

- Pay cash for your vehicle. If you’re making payments you’re probably paying a lot more than you think- in the long run.

- Take public transportation.

- Carpool.

- Don’t buy more vehicle than you need 95% of the time. You can always carshare if you end up needing more horsepower or more seats for a few days a year.

Regarding fancy cars, 99% of people do not care whether you bought a $7,000 car or a $70,000 car. Is putting off retirement really worth impressing the 1% of people you don’t know that actually give a shit? How many years are you willing to work for the privilege of owning that expensive death trap?

These suggestions are a good place to start whether you’re at the dirt-bag, van-life level like we aspire to be, or you’re more into the treat yo’ self kind of lifestyle- there are plenty of ways to save. There’s really nothing more personal than personal finance, so if you really want to optimize your spending and take an honest look at yourself, take a look at your spending.