Retirement is wasted on the old. Old people hate flying, they don’t have nearly enough energy nor stamina to really make the most out of the freedom that comes with never needing to work again. Young people could make much better use of all those years of unhindered adventure. It’s a real tragedy. Don’t fret friends. Together we can help free all those young people that are endlessly toiling away at meaningless jobs. We can do something about this seriously sad state of affairs. Early Retirement is the solution.

Realizing that retiring early is a possibility is like realizing that the Matrix exists. Just knowing of the possibility of early retirement makes early retirement that much more achievable. So go ahead, pat yourself on the back, you are headed in the right direction.

Now it’s time to take the red pill and free yourself.

Another key realization is that in order to change your destiny, you need to change your behavior. You can easily estimate your time to retirement based on your savings rate. If you are spending everything you make or more than you make, you will never retire. If you can achieve a 50% savings rate, that will put you in the range of 10-12 years until retirement. In order to save more, you need to spend less money, or make more money, or both. The principles aren’t complicated, but figuring out which strategy is best for you will likely take some trial and error.

In order to save more, you need to spend less money, make more money, or both.

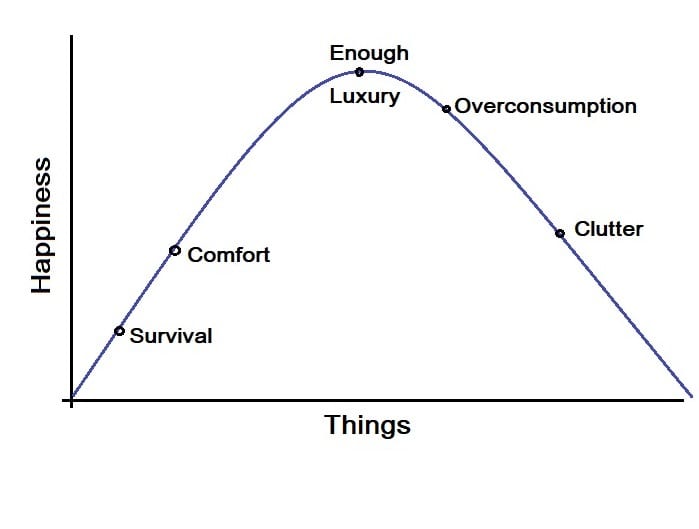

Spend Less

Let the numbers guide you on your journey. Look at your spending and your earning. As you make changes, see what strategies are helping you improve your savings rate. If you’re like most Americans you are likely spending a lot more than you need for a happy life. Try cooking at home more, changing your phone plan, and cutting the cable bill. These small changes will save you money every month, forever. As time has gone on, we have cut out basically everything that didn’t bring us value.

Earn More

This category is HUGE. There are probably an infinite number of ways to improve your earning potential. Side hustles, career changes, starting a small business, investing in real estate, negotiating a raise… If any of these strategies appeal to you, go for it. Investing in ourselves and our small business has been a huge asset on our path to financial independence. We would not have been able to save at this rate if I had continued working in my last career field. We had been on track to retire in our fifties, and now we expect to retire before 40.

Invest Wisely

Invest within tax advantaged retirement accounts first. If your employer offers matching for a 401k or 403b- maximize the match. This is free money from your employer. If you have more to invest, invest within an IRA- an individual retirement account. Buy low fee total market or S&P 500 index funds. We choose Fidelity’s FZROX for investments within our IRAs. See if you are eligible to open a health savings account. Some employers offer these, or you can open one for free at Fidelity but you can only invest if you have a high deductible health insurance plan.

When Can You Afford To Retire?

Traditional retirees can withdraw about 4% of their portfolio per year from their investments. At 4%, stock market growth will outpace your withdrawals- maintaining a nice big cushion to support you throughout traditional retirement. The 4% rule means that you will need 25x your annual living expenses to have enough for you to live on forever. If your cost of living is $40,000 than you will need $1 million. That’s the rule for traditional retiree’s.

25x your annual living expenses will be enough for you to live on forever.

Early retirees can use the same principal but many choose to use a slightly lower withdrawal rate around 3.5%. There are several other strategies that you can employ to lower the risk of outliving your investments and thus allowing you to safely retire on less than 25x your current expenses.

- If you feel like you may be interested in working part time in retirement, the added income can make a huge impact on the total needed within your investments.

- The strategy that we are really excited about is slow traveling in low cost of living areas, essentially halving our cost of living, and using credit card travel rewards to pay for flights. If you are willing to modify your expenses when the market fluctuates, you can minimize your risk of outliving your nest egg. In the case of a market down-turn, you choose to spend your time in a low cost of living area like Thailand, Portugal, or Latin America. Thus halving the amount that you need to take out of the market when stocks dip.

- Another strategy is investing in high dividend funds. Dividends are payments that are paid to shareholders. This allows you to make income from your investment without actually selling any of your assets.

- The bucket strategy consists of keeping money in multiple buckets rather than keeping everything invested in stocks and bonds. To do this you cash out some of your stock when it’s a good price and keep it on hand for upcoming living expenses. This allows you to avoid selling your stock during a market downturn.

We will likely end up employing a combination of these strategies that best fits with our lifestyle and our risk tolerance.

Roth Conversion Ladder

The Mad Fientist is credited with finding this loop hole for the FI community. Goodness it’s a gem. Here’s the step by step from the man himself:

- When you leave your job, immediately roll your 401(k)/403(b) into a Traditional IRA. Since all of these accounts are very similar, tax-wise, this conversion can be done immediately and there are no penalties or tax consequences to worry about.

- If you think you’ll need to access some of your retirement account money in five years, convert the amount you think you’ll need from your Traditional IRA to a Roth IRA. You will pay tax on the amount you convert so make sure you’re in a low tax bracket when performing the conversion and only convert as much as you need.

- Wait five years. While you’re waiting, you can do additional conversions so that you have money to access in years 6, 7, etc.

- After five years, you can take out the amount you converted without paying any additional penalties or taxes (you were taxed in Step #2 when you executed the Traditional-to-Roth conversion).

The Digital Nomad Early Retirement Strategy

Once we get half way to our FIRE number, we plan to take our online business and become digital nomads. We want to travel full time for a while. See the world. Live in low cost countries. At that point, leaving our investment alone for 10 years will allow it to double. Meanwhile our cost of living will half and we will only need a small fraction of our current income to support our nomad lifestyle, any income beyond that we can invest and further shorten our time until full financial independence.

This strategy will allow us to take advantage of the Foreign Earned Income Exclusion. This is a tax rule that means that the first $108,000 of income (per person) is taxed at 0%. That also means that we could convert up to the standard deduction of $12,550 (per person) from our IRA investments into the Roth with a 0% tax rate. Anything beyond that is taxed at the normal income tax rate. In order to qualify for the FEIE you either need to be a resident of a foreign country during that tax year or be living in a foreign country(ies) for 330 days in a 12 month period.

The Foreign Earned Income Exclusion tax rule means your first $108,000 of income (per person) is taxed at 0%.

There are a million other hacks to lower your expenses, save more money, and increase your income. Whichever strategies you employ, remember to let your numbers be your guide, check your income and expenses at least once per month. This will help to motivate you as you track your progress toward your financial goals. This will also help you see which strategies work, and which don’t, and adapt quickly.